Sports' Opportunity for 2021

Sports' Opportunity for 2021

Sports organizations have the chance to test out new techniques to reach non-fans and casual fans, and it might just pay off. Count me in.

Welcome to the Playbook, a weekly newsletter drawing insights from both the performance and business of sports.

There's been quite a bit of discussion about the NFL viewership statistics from Week One. Many articles, including this piece by Michael McCarthy of Front Office Sports, account for the unusually crowded landscape with the US Open tennis, NBA, NWSL, MLS, NHL, Athletes Unlimited, and WNBA happening at once, or believe that it is simply too early to tell. While these impacts may be very real, these numbers can be used to identify potential opportunities for both leagues and teams moving forward.

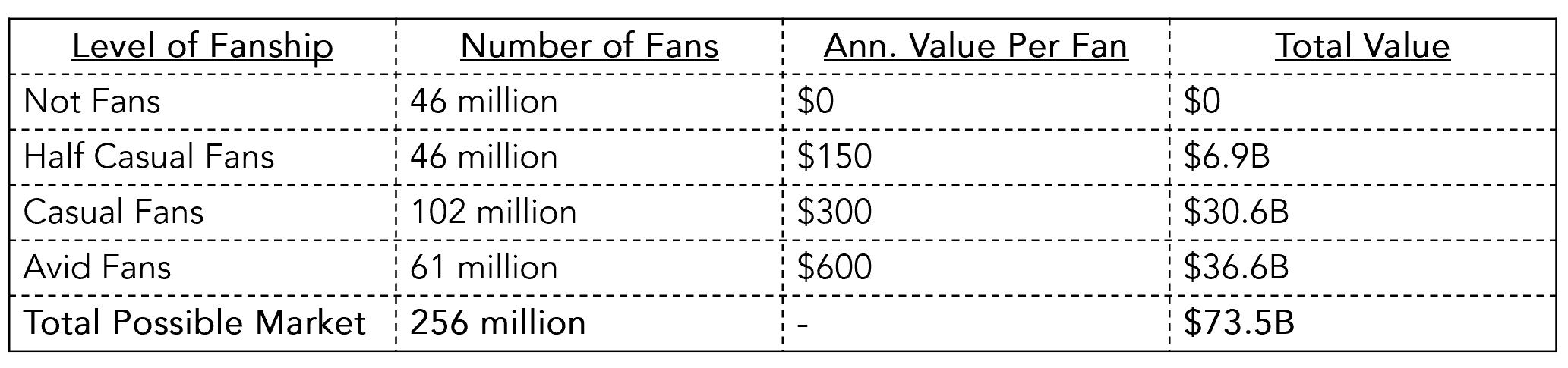

The Market

According to an August 2020 survey conducted by Morning Consult of 2,201 participants, 40% of the respondents consider themselves 'casual fans' and 36% are ‘not fans at all’. That leaves just 24% for 'avid fans'. So, why do sports organizations spend most of their energy on avid fans?

Here’s a simple market sizing graphic, which displays three tiers:

Avid fans (24%): These fans purchase merchandise, hold some level of team membership, and generally can be relied on to support the organization no matter what.

Casual fans (40%): These fans might engage with the organization a few times per week, but do not expect them to spend significantly on the current offering.

Not fans (36%): These people are not fans. They spend on other hobbies/interests.

It’s time for some simple math!

While the survey size cannot statistically account for the entire US population, for this exercise, I will assume that it does. According to US Census data, there are about 256 million people over the age of 18, or adults. Since this discussion is focused on the immediate recovery for the sports industry, adults currently hold the spending power (no slight to the teenagers here).

To keep it simple, let’s say that each category spends at the same rate and the same amount [excluding season ticket purchases]:

Avid fans (24%): $50 per month/$600 per year

Casual fans (40%): $25 per month/$300 per year

Not fans (36%): $0 per month/$0 per year

With 92 million people in the “not fans” category, sports organizations make $0 from their presence in the market. Some may look at these numbers and determine that $66.6 billion dollars is a sizable potential market. Those folks are definitely right - that is a large amount of money coming in to the space. That being said, the COVID-19 pandemic has shown several people that they can find other content to watch without live sports for four months. That should be very scary to sports organizations looking to recover quickly.

There are several possible back-of-the-envelope math equations, but here are just a few to demonstrate why this category and casual fans are crucial to the recovery of the sports industry over the next year:

Scenario 1: Half-Casual. Half of the “not fans” budget $150 for merchandise and other items from a sports organization next year, increasing the possible value of fans to $73.5 billion dollars.

Scenario 2: Casual fans leave. Half of the casual fans have found content on streaming services like Hulu, Netflix, and Amazon Prime Video that is more exciting and/or interesting to watch than sports. The market value drops 22% to $51.9 billion.

Scenario 3: Focused on the possibilities. Sports organizations focus on the key drivers for casual fans to increase their spending. They consider marketing in new places to drive non-fans to casual fanship. There is no need to do the envelope math here because the answer is clear - focusing on non-fans and casual fans will generate much higher additional revenue rather than avid fans (beyond the super fans).

So, there is an opportunity, now what?

Sports organizations need to think about using new channels to market to and cultivate relationships with the 76% of the population who are not avid fans if they want to continue to grow their reach.

Much of the current focus seems to be on avid fans with subscription boxes (below) and fan cutouts. While these types of offerings can drive revenue from avid fans, their exclusivity in both price and availability can be a major turnoff for a casual or non-fan. For example, the Panthers @ Home Membership from the Carolina Panthers has a monthly fee of $65/month plus shipping, which is nearly $800 per year.

To reach casual and non-fans, here are some ideas:

Meet fans where they currently are by leveraging series like Sunderland Til I Die, All or Nothing, Hard Knocks, and Take Us Home: Leeds United. For example, All or Nothing from Amazon Prime Video has covered five NFL teams (Cardinals, Rams, Cowboys, Panthers, Eagles), one college team (Michigan), two Premier League teams (Manchester City, Tottenham), and two national teams (Brazilian soccer team, New Zealand All Blacks). These series show the internal nature of the organization and allow viewers to follow story lines for each member of the team. For example, the team chef for Sunderland, Joyce Rome, was one of the highlights of the entire Til I Die series. Perhaps Joyce could host cooking lessons, or better yet, a discussion on life lessons.

Meeting non-fans where they are through partnerships. DoorDash’s NBA deal (and Postmates with the NFL, to be fair) is a great example of meeting non-fans where they are. In this case, meal delivery is how most people are engaging with restaurants right now, so it’s a great way to reach new fans. For every DoorDash and Postmates, there are several other opportunities to engage with new customers in every sports market.

Tiered subscription models. In addition to the subscription boxes focused on avid fans, organizations can create tiered models where anyone has an opportunity to be a part of the club. One great example of this is Collingwood Football Club from the Australian Football League in Melbourne, Australia. Collingwood provides 28 options for fans to become a member of the club. Their “Support from Home” packages are below, including an international option. The pricing is high because each of the ‘digital insider’ packages include a pass to watch all games, which would not be necessary for a casual fan.

Innovating on merchandise. While many avid fans might be interested in purchasing items with large logos, casual and non-fans will probably be more likely to elect for more subdued options. Sportscaster Erin Andrews’ line for the NFL, WEAR by Erin Andrews, offers these sorts of options to women who might want to represent their team in a more subdued manner. This style does not have to only focus on women, as some men might also prefer to wear more subdued merchandise as well.

Supporting the growth of their athletes’ brands. As the Sports Innovation Lab’s “Fluid Fan” research shows, trends are pointing to people following athletes over teams. Teams could leverage and help grow their athletes’ brands to drive more fans to their organizations. As an example, Greg Olsen’s recently launched podcast on Blue Wire Podcasts offers an inside glimpse into the life of a tight end in the NFL.

Final Thoughts

2020 has been an unexpected year for the sports industry. A long road to recovery is ahead for many organizations to get back to pre-pandemic financial health. Nevertheless, the immediate future is an opportunity to try out new marketing techniques, improve offerings, and innovate for the future. After a testing period, organizations might find that many of these new opportunities are sustainable lines of business for the near term and post-pandemic future.

Enjoyed this article? I also write a weekly newsletter.

Feedback? Questions? Please feel free to comment below, or send me an email at katherine.rowe@utexas.edu.